15 Best Apps Like Sezzle: Top Buy Now, Pay Later Alternatives for 2026

Klarna, Afterpay, Affirm, Zip, and PayPal Pay Later are the strongest alternatives to Sezzle in 2026, each offering interest-free pay-in-4 installments with higher merchant acceptance and more flexible approval processes. Sezzle works well for many shoppers, but its service fees, limited merchant network, and inconsistent customer support have pushed plenty of users to explore what else the BNPL market has to offer.

The buy now, pay later space has matured considerably. What started as a niche payment option for fashion retailers now spans electronics, travel, furniture, groceries, and even healthcare. A Consumer Financial Protection Bureau analysis of BNPL market trends found that the five largest BNPL lenders originated over 180 million loans totaling $24.2 billion in 2021 alone, a figure that has grown substantially since. There are genuine, well-capitalized alternatives worth knowing about before defaulting to any single app.

What Makes Shoppers Look for Sezzle Alternatives

Sezzle splits purchases into four equal payments over six weeks, with the first installment due at checkout. The app supports over 47,000 merchants and offers up to $15,000 in spending power for qualified users. Those are solid numbers — but the friction points are real.

Service fees vary by purchase price, and rescheduling a payment (a feature Sezzle markets as a differentiator) can cost $5 or more depending on your plan. CNBC Select rates it as “best for rescheduling” specifically, which is a narrow niche to occupy in a field where competitors increasingly offer zero-fee flexibility by default.

On r/Sezzle — a community focused on the platform — the complaint thread that surfaces most frequently involves customer service. One user described the experience as “by far the worst payment app ever used,” while several others cited failed payments being processed even after cancellation and difficulty reaching support. These aren’t isolated rants: they reflect a pattern that consistently shows up in Trustpilot and App Store reviews alongside the platform’s genuine strengths.

“Sezzle and their customer service”

— r/Sezzle, multiple recurring threads (2025–2026)

None of that makes Sezzle a bad product. It makes it a product with a specific user profile — and for everyone else, there are better fits waiting.

Apps Like Sezzle: Full Comparison at a Glance

The table below covers the 10 most widely used Sezzle alternatives, ranked by merchant acceptance and overall user satisfaction. All figures reflect 2025–2026 data from publicly available terms and third-party review aggregators.

| App | Payment Options | Interest / APR | Spending Limit | Credit Check | Late Fee | Best For |

|---|---|---|---|---|---|---|

| Klarna | Pay in 4, Pay in 30, Financing | 0% (Pay in 4), up to 33.99% APR (financing) | Up to $10,000 | Soft (Pay in 4) | Up to $7 | Broad merchant coverage |

| Afterpay | Pay in 4, Monthly | 0% (Pay in 4) | Up to $2,000 | Soft | Up to $8 | Fashion & beauty retail |

| Affirm | Pay in 4, 6–60 months | 0% to 36% APR | Up to $20,000 | Soft | None | Large purchases |

| Zip | Pay in 4 | 0% | Up to $1,500 | Soft | Up to $7 | Bad credit, flexibility |

| PayPal Pay Later | Pay in 4, Pay Monthly | 0% (Pay in 4) | Up to $1,500 | Soft | None | Online shopping everywhere |

| Splitit | 2–36 monthly installments | 0% (uses existing credit) | Your credit card limit | None | None | No new credit line needed |

| Perpay | Up to 6 months | 0% | Up to $1,000 initial | None | None | Paycheck-linked payments |

| Paidy | 3-month installments | 0% | Varies | Soft | Varies | Japan-based shopping |

| Zebit | Up to 6 months | 0% | Up to $2,500 | None | None | No credit check shoppers |

| ViaBill | Monthly installments | 0% | Varies | Soft | Varies | Subscription & service purchases |

Top 8 Apps Like Sezzle: In-Depth Reviews

Not every BNPL app deserves equal consideration. The eight below earned their positions through merchant reach, fee transparency, and real user outcomes, not marketing budgets.

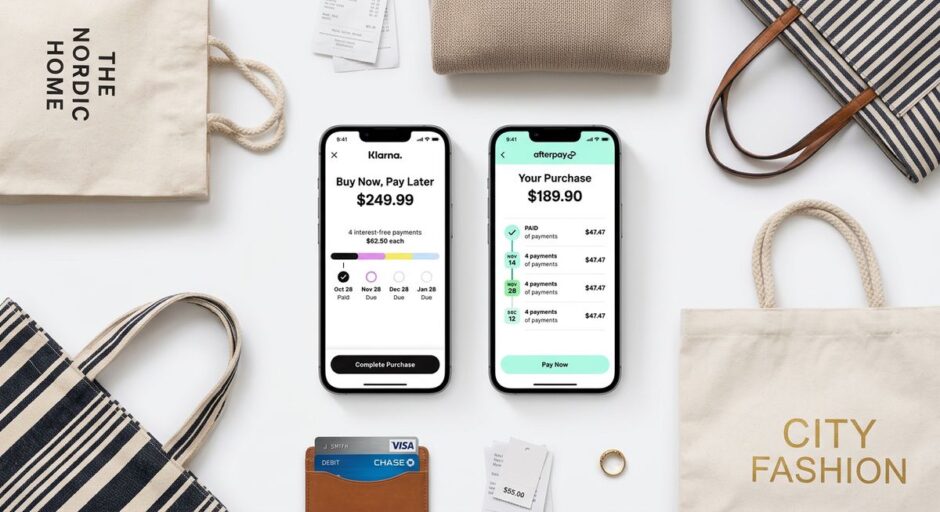

1. Klarna, Best Overall Sezzle Alternative

Klarna operates in 45 countries and partners with over 500,000 merchants globally, making it the most accessible BNPL option for most US shoppers. The pay-in-4 product splits any purchase into four equal payments every two weeks at 0% interest. No late fee is charged on the first missed payment; subsequent missed payments incur up to $7.

What sets Klarna apart from Sezzle is flexibility beyond pay-in-4. The “Pay in 30” option lets you receive your order, inspect it, and pay in full within 30 days, particularly valuable for online clothing purchases where returns are common. Klarna also offers longer-term financing at rates up to 33.99% APR for larger purchases, though those longer plans involve a hard credit check.

Klarna’s app (rated 4.8 on the App Store with over 2.8 million reviews) integrates a built-in shopping browser with cashback offers, price drop alerts, and shipping tracking. The breadth of that ecosystem is where Sezzle’s more transactional experience starts to feel thin by comparison.

2. Afterpay, Best for Fashion and Beauty

Afterpay pioneered the pay-in-4 model before Sezzle existed, and its merchant network in fashion, beauty, and home goods remains unmatched among BNPL apps. The platform reports around 22 million active customers globally, with Square (its parent company since 2022) integration giving it deep penetration in smaller and mid-size US retailers.

Spending limits start low, often $50 to $150 for new users, and scale quickly with on-time payment history. The ceiling reaches $2,000, which covers most everyday purchase categories without triggering an underwriting process. No interest ever applies to pay-in-4 orders; late fees cap at $8 or 25% of the order value, whichever is lower.

Afterpay introduced a “Monthly Payments” option in 2024 for purchases up to $4,000, giving it some of Affirm’s range without requiring a separate application. That range makes it a more complete Sezzle replacement than a pure pay-in-4 competitor.

3. Affirm, Best for Large Purchases

Affirm serves a different segment than Sezzle’s core use case. While most BNPL apps focus on purchases under $500, Affirm supports financing from $50 to $20,000, with repayment terms stretching from pay-in-4 to 60 months. That makes it the right tool for mattresses, appliances, travel bookings, and electronics, not impulse buys at online boutiques.

The fee structure is unusually transparent: Affirm charges 0% APR for standard pay-in-4 orders at participating merchants and between 0% and 36% APR for monthly plans. Critically, Affirm never charges late fees. A missed payment costs nothing beyond potential credit bureau reporting (Affirm does report payment history to Experian for monthly plans, which can help or hurt your credit score depending on your behavior).

According to Affirm’s 2025 annual report, the company processed $26.6 billion in gross merchandise volume in its fiscal year 2025, a scale that gives it negotiating power most competitors can’t match. The result is acceptance at major retailers including Amazon, Walmart, Target, Peloton, and hundreds of travel platforms.

4. Zip, Best for Shoppers with Limited Credit History

Zip (formerly QuadPay) runs on a virtual card model that works at any merchant accepting Visa, not just Zip’s partner list. That single feature eliminates the biggest pain point with Sezzle and other closed-network BNPL apps: the frustration of arriving at checkout only to find your preferred payment app isn’t accepted.

The approval process is notably lenient, with Zip performing only a soft credit check and approving applications based on factors beyond traditional credit scores, including spending patterns and repayment history within the app. Spending limits start at $250 and can reach $1,500. The $1/payment convenience fee ($4 total per transaction) is charged regardless of whether you pay on time, an unusual structure compared to competitors who only charge if you miss a payment.

Zip’s App Store rating of 4.9 stars from 798,000+ reviews reflects genuine user satisfaction, particularly among shoppers with thin credit files who struggle to get approved elsewhere. The app’s 4-installment structure matches Sezzle exactly, making the switch straightforward.

5. PayPal Pay Later, Best for Broad Online Acceptance

PayPal Pay Later’s competitive advantage is distribution. With PayPal accepted at 29 million merchants worldwide, the pay-in-4 option appears at checkout wherever PayPal exists, no merchant partnership required. For online shoppers, that universality removes the guesswork entirely.

The pay-in-4 product charges 0% interest, no late fees, and performs only a soft credit check. PayPal also offers a “Pay Monthly” option for purchases $199 to $10,000, with APR between 9.99% and 35.99% and repayment terms of 6, 12, or 24 months. Unlike Sezzle’s opaque service fee structure, PayPal’s pricing is straightforward: free if you pay on time, with late fees on monthly plans only.

The main limitation is that PayPal Pay Later is unavailable at merchants who don’t accept PayPal at all, an increasingly rare scenario for online shopping, but still relevant for smaller merchants using alternative payment processors.

6. Splitit, Best for Existing Credit Card Holders

Splitit operates on a fundamentally different model: instead of extending a new line of credit, it temporarily holds funds on your existing Visa or Mastercard and charges each installment against that card as it comes due. No application, no credit check, no separate account, your credit limit is the spending limit.

That structure makes Splitit uniquely valuable for shoppers who have existing credit availability but want to preserve cash flow. The interest question answers itself: whatever rate your credit card charges applies to any balance you carry, but if you pay your card statement in full each month, Splitit costs nothing. Merchants pay Splitit’s processing fees, not consumers.

Merchant acceptance skews toward premium retailers, luxury goods, high-end furniture, healthcare providers, and travel operators. For those categories, Splitit competes with Affirm rather than Sezzle, but shoppers leaving Sezzle for high-value purchases will find it a cleaner fit than traditional BNPL apps.

7. Perpay, Best for Paycheck-Linked Installments

Perpay routes payment through payroll: users link their bank account, set a payment amount, and Perpay automatically deducts installments on payday. No credit check. No interest. No late fees because the payment structure makes missing a payment essentially impossible. The initial spending limit is up to $1,000, growing over time with consistent payment history.

The constraint is that Perpay operates its own marketplace rather than a network of third-party merchants. That means product selection is curated rather than unlimited. For shoppers primarily buying electronics, home goods, and furniture, the selection is sufficient. For someone replacing Sezzle across dozens of different merchant categories, Perpay serves as a complement rather than a full substitute.

Perpay also reports payments to credit bureaus, which makes it a rare BNPL option that actively builds credit history, meaningful for users who want their payment discipline to show up somewhere beyond the app itself.

8. Zebit, Best with No Credit Check Required

Zebit requires neither a credit check nor an existing credit card. The broader BNPL category has increasingly segmented into credit-check and no-credit-check tiers, with Zebit firmly in the latter. Eligibility is based on income verification alone: applicants must show stable employment and a U.S. bank account. Approved users receive up to $2,500 in spending power, repaid in installments over up to six months at 0% interest.

Like Perpay, Zebit operates a proprietary marketplace with curated products. The selection covers major consumer electronics brands, furniture, appliances, and sporting goods. Zebit’s target user, someone who has been declined by every other BNPL app, will find the product library narrower than they’d like but the approval process meaningfully more accessible than alternatives.

Fee Breakdown: Sezzle vs. Top Alternatives

Fee transparency is where BNPL apps differ most significantly, and where Sezzle has the most room to improve. The table below compares the total cost of a $300 purchase paid in four installments across six platforms.

| App | Service / Convenience Fee | Late Fee | Total Cost ($300 purchase) | Transparent Pricing? |

|---|---|---|---|---|

| Sezzle | Varies (up to ~5% of order) | Up to $10 | $300–$315+ | Partial |

| Klarna | None (Pay in 4) | Up to $7 | $300 | Yes |

| Afterpay | None | Up to $8 | $300 | Yes |

| Affirm | None | None | $300 | Yes |

| Zip | $1 per payment ($4 total) | Up to $7 | $304 | Yes |

| PayPal Pay Later | None | None (Pay in 4) | $300 | Yes |

For a $300 purchase, the difference between Sezzle and a zero-fee competitor can reach $15 or more. Across a year of regular BNPL use, that difference compounds significantly. Affirm and PayPal Pay Later are the only two major platforms that charge neither service fees nor late fees on standard pay-in-4 plans.

Choosing the Right Sezzle Alternative for Your Situation

The strongest BNPL alternative depends on your specific use case rather than any single app’s marketing claims. Below are the situations most users encounter and which alternatives serve them best.

You want the widest merchant coverage: Klarna and PayPal Pay Later. Klarna’s 500,000+ merchant network and PayPal’s 29 million acceptance points cover virtually every online retailer.

You’re financing a large purchase ($1,000+): Affirm. Its $20,000 limit and flexible 6–60 month terms are built for this scenario. No other major BNPL app matches that range with equivalent fee transparency.

You have bad credit or limited history: Zip or Zebit. Zip uses soft checks and non-traditional approval criteria. Zebit requires no credit check at all, just income verification.

You already have a credit card and don’t want a new account: Splitit. It uses your existing credit line with no application, no hard pull, and no new debt relationship.

You want to build credit through BNPL payments: Perpay or Affirm (monthly plans). Both report payment history to credit bureaus, making them productive for anyone actively managing their credit file.

You’re primarily buying fashion, beauty, or home decor: Afterpay. Its merchant relationships in these categories are unmatched, and the spending limit structure is optimized for the typical purchase sizes involved.

Frequently Asked Questions

What are the best overall alternatives to Sezzle?

Klarna, Afterpay, and Affirm consistently rank as the strongest Sezzle alternatives based on merchant acceptance, fee transparency, and user satisfaction. Klarna offers the broadest merchant network; Afterpay leads in fashion and beauty retail; Affirm is the top choice for purchases over $1,000 that benefit from flexible multi-month repayment.

Which BNPL app has the lowest fees?

Affirm and PayPal Pay Later charge zero fees on standard pay-in-4 plans, no service fees and no late fees. Klarna and Afterpay charge late fees only when a payment is missed (up to $7 and $8 respectively) but nothing upfront. Zip charges $1 per installment as a convenience fee regardless of payment timing, making it the most predictable-cost option even if not the cheapest.

Can I use multiple BNPL apps at the same time?

Yes. Each BNPL app maintains its own account and credit relationship, so there’s no technical barrier to using Klarna for one purchase and Affirm for another simultaneously. However, multiple BNPL commitments increase your total monthly payment obligations. Apps that report to credit bureaus (Affirm’s monthly plans, Perpay) will factor all reported balances into your credit profile.

Which BNPL app is easiest to get approved for?

Zip, Zebit, and Perpay have the most accessible approval processes. Zip performs only a soft credit check and uses non-traditional factors in its decision. Zebit and Perpay require no credit check whatsoever, Zebit uses income verification alone, and Perpay links directly to payroll. New users with no credit history or past credit problems typically have the best results starting with one of these three.

Do BNPL apps hurt your credit score?

Most pay-in-4 BNPL apps perform soft credit checks that don’t affect your score. Affirm’s monthly financing plans involve a hard inquiry that can temporarily reduce your score by a few points. Affirm (monthly plans) and Perpay report payment history to credit bureaus, which means on-time payments build positive history while missed payments can cause harm. Klarna, Afterpay, and PayPal Pay Later do not report pay-in-4 activity to credit bureaus.

What’s the main difference between Sezzle and Klarna?

Klarna has substantially broader merchant acceptance (500,000+ vs. Sezzle’s 47,000+), offers more payment products beyond pay-in-4 (pay in 30 days, long-term financing), and charges no service fees on standard purchases. Sezzle’s main differentiator is its rescheduling feature, which Klarna doesn’t offer in the same form. For most users, Klarna’s wider network and fee structure make it the stronger default choice.

Which BNPL app has the highest spending limit?

Affirm offers the highest spending limit at up to $20,000, making it the only mainstream BNPL app that covers large furniture sets, appliances, and home improvement projects. Klarna follows at up to $10,000 for qualified users. Splitit’s effective limit is your credit card’s available balance, which can exceed both if you carry a high credit limit.

Are there BNPL apps that don’t do any credit check?

Zebit, Perpay, and Splitit perform no credit check at all. Zebit and Perpay use income-based underwriting instead. Splitit requires no underwriting because it uses your existing credit card rather than extending new credit. Zip performs only a soft credit check that doesn’t affect your score.

The BNPL Market Has Moved Past Pay-in-4

Sezzle launched at a moment when splitting a purchase into four payments felt novel. Five years later, that feature is table stakes, and the differentiation has moved to fee transparency, merchant coverage, credit building, and flexible repayment options that extend well beyond six weeks.

Klarna and Afterpay lead on breadth. Affirm leads on range and fee honesty. Zip and Zebit serve users traditional credit products have left behind. Splitit solves the problem for people who already have credit capacity but want better cash flow management. None of these apps is perfect for every buyer, but each solves a specific problem better than any other option on the market.

The shopper who takes time to match their use case to the right platform will spend less, get approved more reliably, and interact with fewer frustrating customer service teams than anyone who defaults to the first BNPL app they encounter.